In the summer of 2000 the LSE introduced three main types of auction: closing, opening and intra-day, as a refinement to the SETs order book, that had successfully replaced the market-making based system of trading for the top 200 or so stocks.

A number of opportunities for CFD traders regularly occur in these auctions, particularly the opening and closing auctions. For instance, the London Stock Exchange starts each trading session with a ten-minute pre-market auction from 7.50am to 8.00am and participating allows you to take advantage of RNS announcements. The closing auction occurs for a five-minute period from 16:30 to 16:35 after the close of normal trading. The reason for this is that the auction process suspends trading for five minutes and allows participants to submit orders to buy and sell at a stipulated price. Throughout this five-minute period, a theoretical ‘uncrossing’ price is calculated continuously and dynamically and displayed. At the end of the five-minute period, any orders that can be completed are matched up and executed at one specific price, the uncrossing price.

The key difference between the auction period and normal trading is that participants can input orders to buy or sell ‘at market’. This instruction can create short-term imbalances in liquidity that in turn forces stock prices up or down. CFD traders can take advantage of these imbalances by submitting orders in the opposite sense to secure the best prices; quite regularly the daily high or low for a stock will occur in the auction. Those traders not accessing these prices are missing out on optimum dealing prices, an important factor for short-term traders.

The charts in this article illustrate the kind of surge in stock price that can occur in the auction when ‘at market’ orders are placed where there is a limited amount of liquidity available.

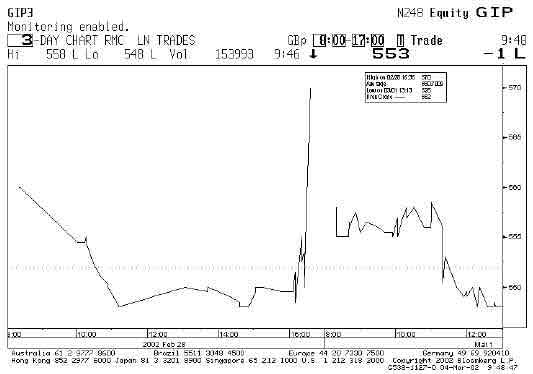

The two-day chart for RMC Group (RMC) at the end February above is a good example of what can happen when a large ‘at market’ buy order is placed in the post-market auction. Here the price is forced up and 81500 shares uncross at 570p. This presents two potential opportunities to the CFD trader. Firstly, if he was long the CFD in RMC originally, he can sell his long position at an extremely favourable price in the context of the day’s trading rage (547p-560p).

Secondly, and perhaps more importantly, he can elect to open a CFD short position by selling in the auction (to open) at 570p, providing liquidity to offset the ‘at market’ buying order. If he was comfortable selling down to say 560p, he could submit an order to sell at this level, increasing his chance of execution.

As all uncrossing takes place at the same price, if the uncrossing price were still 570p, he would complete his order at 570p, an improvement on the 560p level submitted. If however, the uncrossing price were 558p, he would not end up executing at all, as his sell order was submitted above this. This demonstrates quite well the balancing act that CFD traders must perform to extract the best price while ensuring a fill.

As can be seen, RMC reverted back to its previous day’s trading range the next morning, providing ample opportunity to close the short position between 550p and 555p. Three or four percent may not sound much to a long-term investor but to a CFD trader it provides a useful return on a relatively short-term overnight trade.

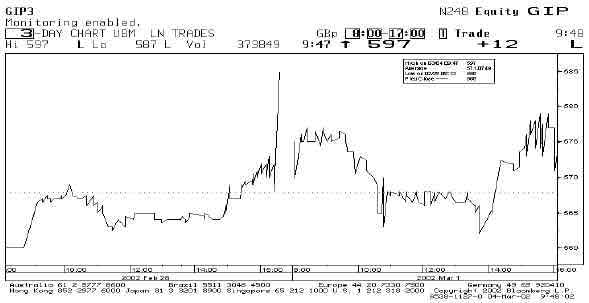

A similar situation can be seen to occur in United Business Media (UBM) on the same day in late February. The two-day chart below shows the spike in the price of UBM when an ‘at market’ buy order for 240,000 UBM was submitted in the closing auction forcing the uncrossing price up to 585p.

Having traded during the day between 560p and 572p this proved an attractive level at which to sell or short the CFD, and the next day the stock reverted to a more normal level, providing those CFD traders prepared to take overnight risk, a healthy return. Stocks that should possibly be avoided in this strategy are those involved in special situations (takeover talks for instance), those companies reporting results the following trading day or those going ‘ex-dividend’ (usually only on Wednesdays). A list of stocks reporting and ex-dividend dates are easily obtained from a number of financial websites.

Another example occurred on 17 January when Wolseley, the specialist trade distributor of plumbing and heating products, issued its trading statement for the five months to 31 December. The favourable figures were released at 7am. The market reaction was positive and traders with DMA were able to capitalise on this during the opening auction, which saw the stock rise from its Friday close of 988p to open on the Monday at £10.15. The positive reaction to the trading statement was such that it persisted past the opening auction and into the trading day itself. Opening on 17 January at £10.15, the price went on to rise to just under £10.55 a little after 10am before finishing the day at £10.46-£10.4750.

Although at first sight, placing ‘at market’ orders in the auction may seem an inefficient means of execution, there can be a number of reasons for their use. Firstly, the client, for whatever reason, may stipulate that he wishes to trade in the closing auction only, thereby ensuring dealing at the closing price for the stock on the day. Secondly, the order may be part of a bigger, ‘worked’ order that is being executed in tranches throughout the day, a third in the morning, a third in the afternoon and a third in the closing auction for instance.

Direct Market Access and Auctions

If you are prepared to do the research, market auctions can provide the best reason for you to switch to a CFD provider who offers direct market access (DMA). There are pros and cons about having DMA, the main disadvantage being the ongoing additional cost which you must balance against the advantages of faster and more transparent execution. But Level II market access allows access to the current outstanding orders, both bid and ask prices, together with the volumes requested. This means that apart from speed, there is the potential for improved pricing when compared to the relatively static quote-driven service.

Participation in the auctions is restricted to those with DMA. Thus if you have DMA, then you can participate in the London Stock Exchange (LSE) auctions which take place at both the opening and the closing of the market. Even though there is no actual trading in these periods (which are before the market opens and after it closes), you are still able to place and delete orders. The trades are worked out at the end of the auction period. Auctions are often seen as the most volatile and liquid periods of the day, which makes trading Small Caps (or stocks with wide spreads) even more appealing. Often during the auction periods the stock achieves its high or low of the day, and the only way to benefit from this is to take part in the auctions.

If no transactions take place during the auction period, you may be wondering how it works and how you can benefit, even with DMA. The answer is in the system of ‘uncrossing’ all the orders entered at the end of the auction. In particular day traders with DMA Access are able to take advantage of the pre-opening auctions of the exchange to place orders in advance of the opening of the market – commonly for taking advantage of RNS announcements. Orders placed during these periods appear on the Level 2 screen, along with the indicative uncrossing price updating in real-time as calculated by the exchange. This is because during the auction period, an uncrossing price is continuously calculated and displayed (although no actual orders are processed during the auction period), and after the auction ends, all orders are fulfilled at the single uncrossing price. This is the price that would allow the maximum volume to be executed where a share is crossed, in particular where a buy order has an equal or higher-priced sell instruction. At 8.00am every stock that is crossed will begin to uncross at a single uncrossing price. This is the official opening price for the trading session and could be at a different level from the previous night’s close. Likewise, no order execution actually takes place during the closing auction, instead all crossed trades go through at the final official uncrossing price as soon as the auction period comes to an end.

Taking part in this process is similar to being a market maker. The reason that daily highs or lows are seen at the auction is that there are short term imbalances in the liquidity because of the entered orders, and these force the prices to change up or down, often outside the usual daily range.

If you are a CFD trader with access to see what is happening in the auctions, you may be able to profit fairly simply. Say that a share price has risen above its normal daily range through the actions of the auction. Seeing this, you can submit a CFD order against the move. To do this you can open a short CFD position at or near the price. Depending on the level, it may or may not be executed, as this will depend on the uncrossing price finally decided by the exchange. If it is executed at a high price, as submitted, then it is easy to close the position during normal trading, when the regular range of the price has been re-established, and this will net you a quick profit. Quite a number of times a liquidity imbalance arises during the auction that offers the possibility to be filled at a significantly better price than is available during the rest of the trading session. This applies especially for a small cap that issues results that differ significantly from expectations ahead of the start of the opening auction.

Another way that you can make gains is if you are already in a long CFD position for the shares. You can enter an order to sell your long position during the auction period, when the price is inflated, and again if executed you will make more profit than waiting for the open market price. In some ways it is a balancing act to select a price that will be executed, but if you choose wisely you can find this an easy source of extra profits.