I want to discuss the recent trend of companies’ shares in bankruptcy or near bankruptcy skyrocketing without any clear reason. I’m referring to buying stocks like Gamestop Corp, AMC and even Hertz. This trend may be due to a feedback loop between momentum, quantitative, and retail traders. However, this trend is odd because the company’s bonds are trading at a severe discount to par value, indicating little-to-no value for equity holders after the company reorganizes under American bankruptcy law.

Buying Equity in Companies with Debt Priced at Distressed Levels is a Losing Strategy

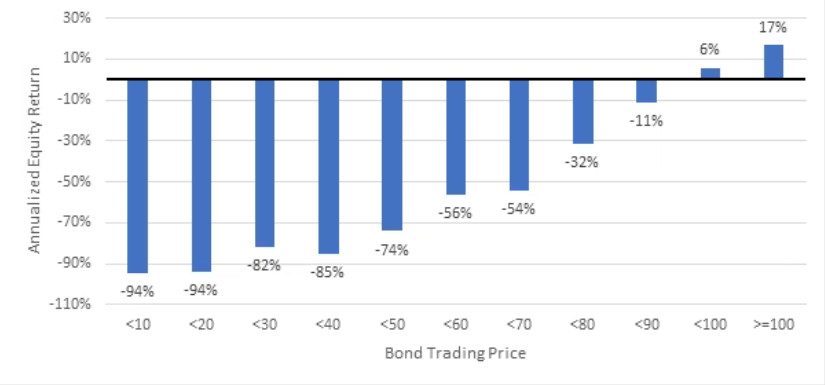

Quantitative asset manager, Verdad Cap, based out of Boston, has run numbers on the equity returns of leveraged companies, both investment-grade and junk, whose dollar bonds trade at distressed levels. For example, purchasing the shares of companies whose fixed-income securities trade at under 10 cents on the dollar, or between 10 and 20 cents on the dollar. The data set goes back to 1996, and Verdad’s director of credit, Greg Obenshain, has found that bondholders are rarely wrong. While there is a possibility that bondholders could be wrong, the data suggests that it’s not very often.

The dataset goes way back 1996

And this is what he found:

The point is that historically *IF* you purchased a portfolio of shares in companies whose bonds traded at under 70% of par but greater than 60% of par then you could expect to lose 54% overall.

But that’s on a portfolio basis. So some will do well whilst others will do poorly.

This looks bad, but at least we can understand what retail is trying to do here: “buy cheap equities that the market hates.”

Buying stocks of heavily indebted companies is normally a bad strategy even if the stock is trading at a very low level. You might hope that a knight in shining armour would launch an opportunistic bid but bidders rarely buy the equity of companies that are in financial distress, they buy the debt. Who wants to takeover a company with losses and cash burn? Ask Mike Ashley of Frasers Group PLC, he knows that now, although it cost him £150m to learn that lesson with Debenhams. I would advise anyone who doesn’t know what covenants are not to invest in companies that have large amounts of debt!