06/07/2023

It is interesting to reflect on today being the anniversary of the US yield curve inversion (2 year versus 10 year). After 1 year, the yield curve inversion has generally increased and is now about 1.08%, meaning it costs 1.08% more to borrow for 2 years than 10 years. Such a yeld curve inversion has resulted in a recession following every time since WWII I believe. This is also the largest inversion of the yield curve since August 1981 from what I can see. In the UK 10-year gilts have now gone to 4.5% again, the same level as the fiasco budget last year.

UK stocks are cheap that’s for sure and smallcap stocks even cheaper. However, what happens in the US ultimately drives global markets (including the UK) and I’m a bit concerned that global investors are torn between a shallow global recession and talk of “this time is different” (i.e. the yield curve inversion won’t lead to a recession because the Fed have perfected their game). I am still very cautious about the impact of “toppy” US markets (with AI the latest bubble and the US having an 80s Japan style c60% share of the Global market) and that’s leading me to hold back in the UK small cap space. I know its difficult / virtually impossible to time markets, but…..what do others think?

11/03/2023

With the accumulation of negative economic and financial news, there is growing apprehension about an impending recession. Market participants and clients are understandably worried about the possibility of a prolonged, severe downturn. Although we cannot predict the future, we share in their concern and are troubled by the current state of affairs. It is not our intention to predict a recession, but we acknowledge the possibility.

There are a number of commonly monitored metrics that suggest an increased likelihood of a recession. In the following discussion, we will examine these indicators and what they might signify.

Inflation and Interest Rate Hikes

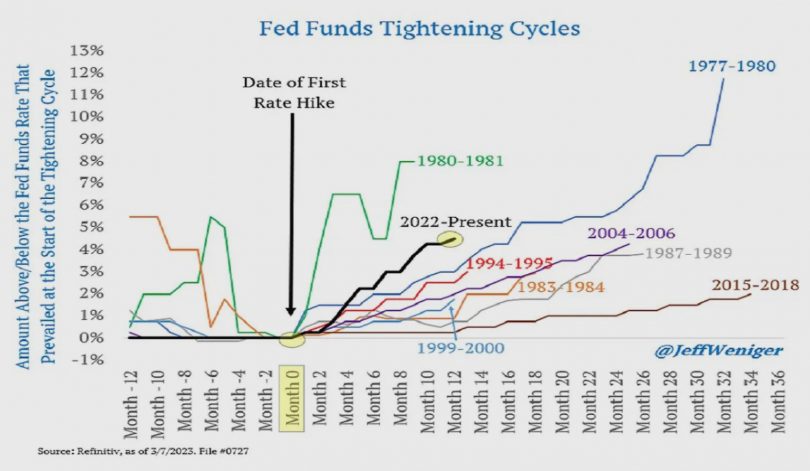

In an effort to control rising inflation, the Federal Reserve has been actively increasing the federal funds rate.

Fed Interest Rate Hikes

As evident from the information above, the current tightening cycle in the US is among the most forceful seen in many years. Federal Reserve Chair, Jerome Powell, has indicated that if inflation persists, the Fed may proceed to increase rates at a faster pace, potentially surpassing their original target range of 5-5.5%. This raises uncertainty around the duration of the hiking cycle and when it may ultimately come to an end.

In past occurrences, an abrupt increase in interest rates by the Fed to combat inflation has preceded a recession. It is important to recognize that a significant number of investors and economic participants, who had anticipated a “Fed pivot” earlier in the cycle, were taken by surprise by the Federal Reserve’s determination to persist with raising rates to address inflation. As a result, many of these participants are currently ill-equipped to cope with the elevated cost of capital.

Yield Curve Inversion

The yield curve that has garnered the market’s attention is the differential between 2-year and 10-year US government bonds. An inverted yield curve occurs when short-term bond yields are greater than long-term bond yields. This phenomenon may be indicative of investor apprehension that long-term rates will decrease in response to an economic downturn, with higher short-term yields serving as a hedge against this possibility. In the past, an inverted yield curve has typically signaled the peak of an economic cycle and has been a leading indicator of a U.S. recession with a significant degree of accuracy. As such, it is prudent to closely monitor the yield curve.

In July 2022, the yield curve underwent an inversion, and since then, it has been steepening. As of now, the difference between the 10-year and 2-year yields stands at around -1%, representing a 30-year low. Bloomberg has estimated that based on the current slope of the yield curve, the likelihood of a recession is 71%.

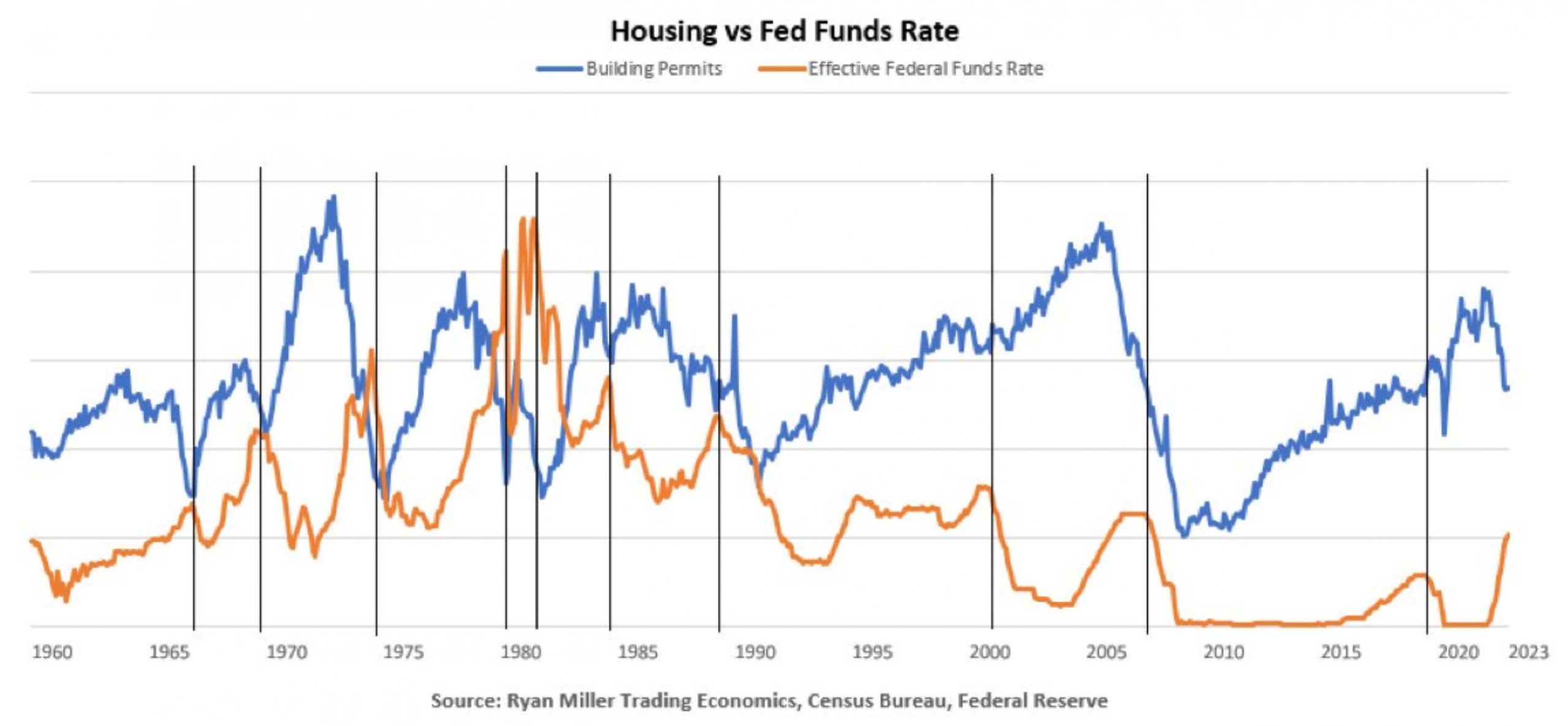

Housing Market Deterioration

The state of the housing market serves as a significant indicator of consumer and overall economic well-being. For the average person, a substantial portion of their wealth is tied up in the equity of their home, and the construction industry is a significant source of employment. Consequently, a decrease in real estate prices and construction activity can be used to evaluate the health of the economy. Real estate prices and building activity reached their peak in mid-2022, but have since been declining, primarily in response to the upward trend in interest rates.

The increase in interest rates not only impacts the construction industry, but also poses challenges for individuals looking to own a home, as it results in higher interest payments. This, in turn, reduces the amount of available capital for purchasing homes, further pushing down prices. As shown below, US housing affordability has reached a multi-decade low.

Commercial Real Estate

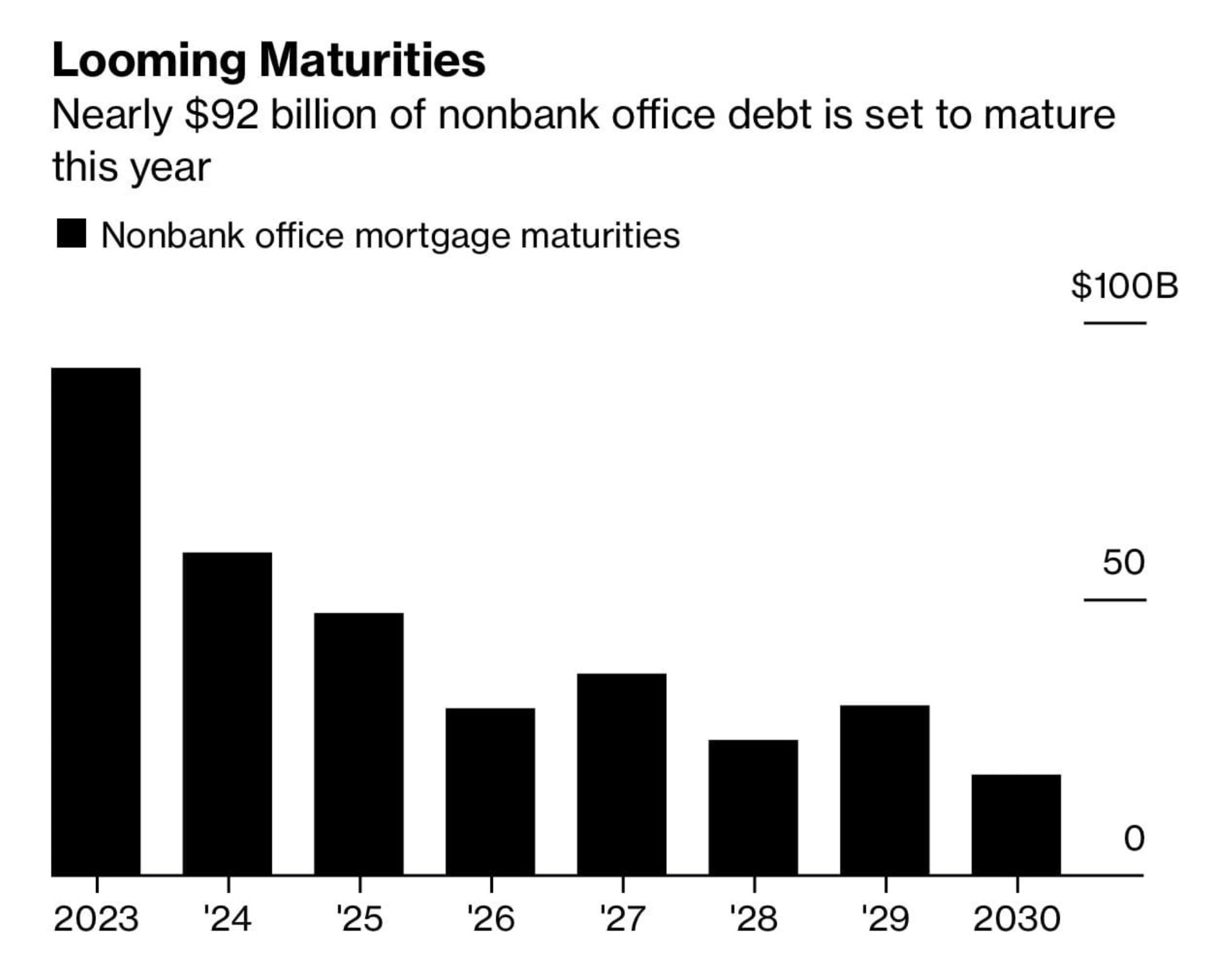

The commercial real estate market, valued at around $21 trillion, is also experiencing significant strain due to the increase in interest rates and the rise in remote work arrangements. Office buildings, in particular, are facing considerable challenges, as the shift towards remote work following the pandemic has negatively impacted their revenue. Additionally, nonbank office debt worth $92 billion is set to mature this year, further exacerbating the situation.

Risk of Broader Financial Contagion

The escalation in interest rates is placing substantial pressure on the financial institutions’ balance sheets, which is elevating the possibility of a more extensive market contagion akin to previous financial crises. The impact of higher rates is already visible in the form of a crack in the financial system, with Silicon Valley Bank, which focuses on technology, experiencing a serious bank run that ultimately led to its demise.

During the tech boom in 2020 and 2021, Silicon Valley Bank’s deposits experienced a significant surge. The bank primarily invested these funds in long-term U.S. treasuries and mortgage-backed securities. However, as the Federal Reserve began increasing interest rates, the value of these bonds decreased, leading to mark-to-market losses of $2 billion and a deficit in capital. This situation triggered a liquidity crisis, with depositors rushing to withdraw their funds from the bank, further exacerbating the problem.

Silicon Valley Bank is not the only financial institution that has invested a significant portion of its deposits into U.S. treasuries and mortgage-backed securities. Many other banks have done the same, and are thus highly exposed to duration risk stemming from the increase in interest rates. Given the interconnectedness of financial institutions, the risk of financial systemic issues is elevated.