by Ming Zhao

26/03/2023

Soon you will hear a lot more on Commercial Real Estate.

Why? Because US banks & PE firms are headed for real estate doomsday.

4 collapses in 11 days

$270B in Commercial Real Estate loans due end of year.

$3B+ defaulted in March 2023 alone

What is Commercial Real Estate & Why Does it Matter?

“Commercial real estate” = Property for Business

The US Commercial Real Estate industry is a $20.7 trillion market.

Core segments include:

– office

– industrial

– multifamily

– retail

– hotels

– land

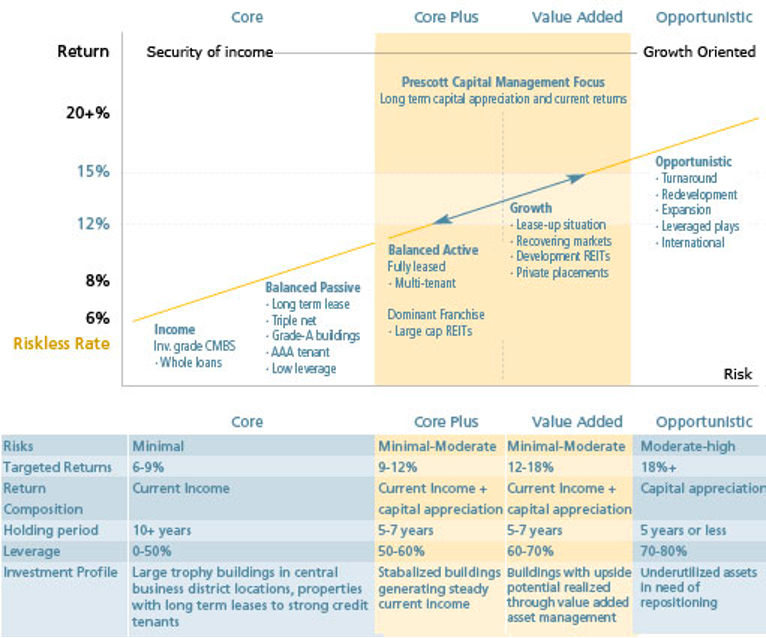

Investors specialize into 3 major investment strategies:

– Core

– Value add

– Opportunistic

Core:

– low risk, “steady income” play

– safe geos (NYC, SF)

– high starting occupancy

– target IRR: 6-9%

Value add:

– medium risk, “asset appreciation” play

– investor must put in work (e.g. make repairs, grow occupancy rate)

– target IRR: 12-18%

Opportunistic:

– high risk

– original asset fucked, this is basically distressed equity/ activist investing

– target IRR: 18+%

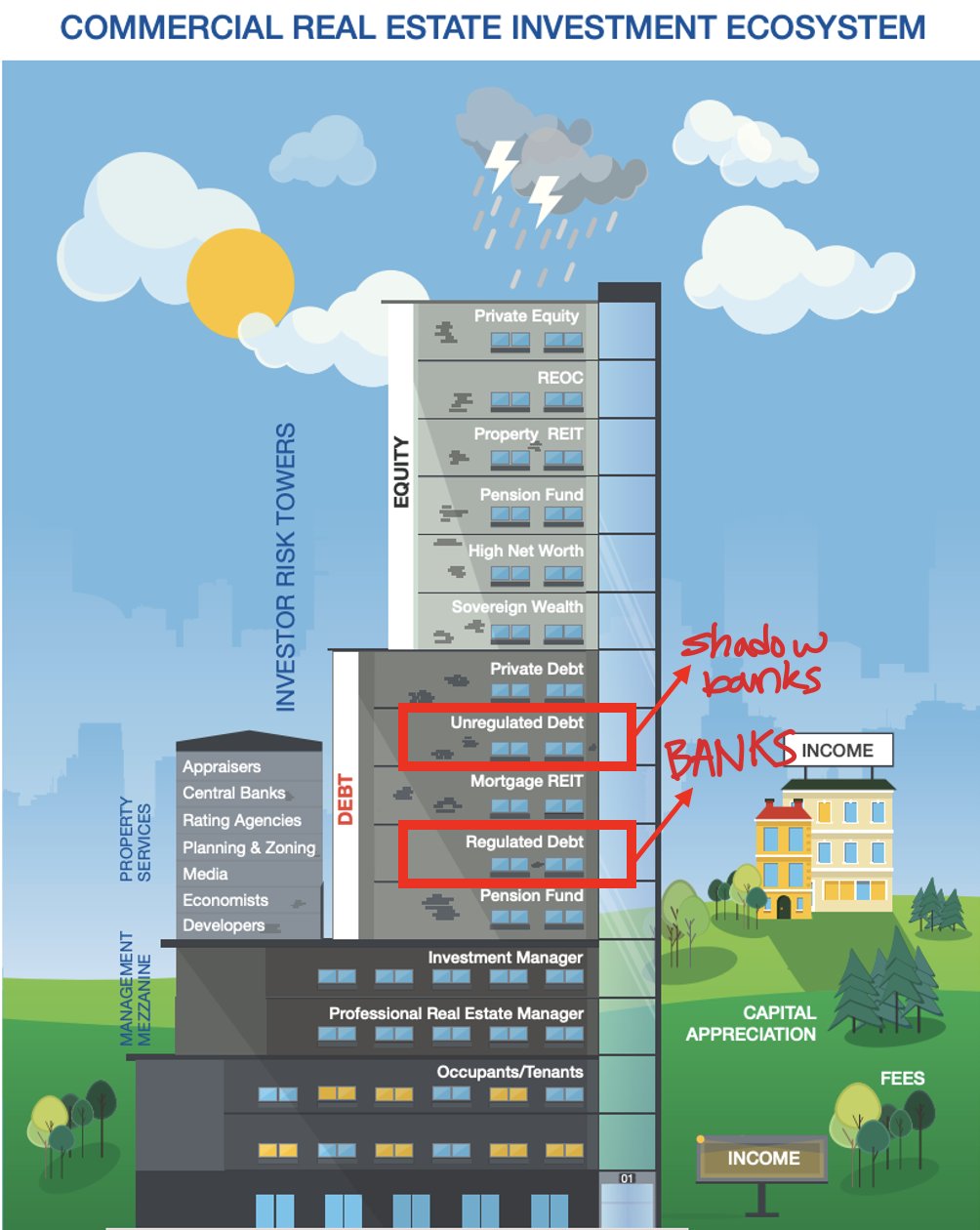

Ways to Invest in Commercial Real Estate

1. Directly buy property & manage (or outsource to mgmt corp) — a CRE equity investor

2. Originate or buy CRE loans — a CRE debt investor

3. Invest in a property REIT (which does #1) or a mortgage REIT (which does #2)

What’s going on in 2023 — Banks’ Current Exposure

Here’s the problem:

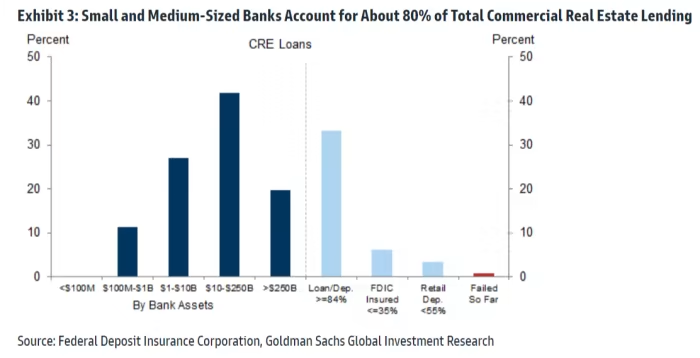

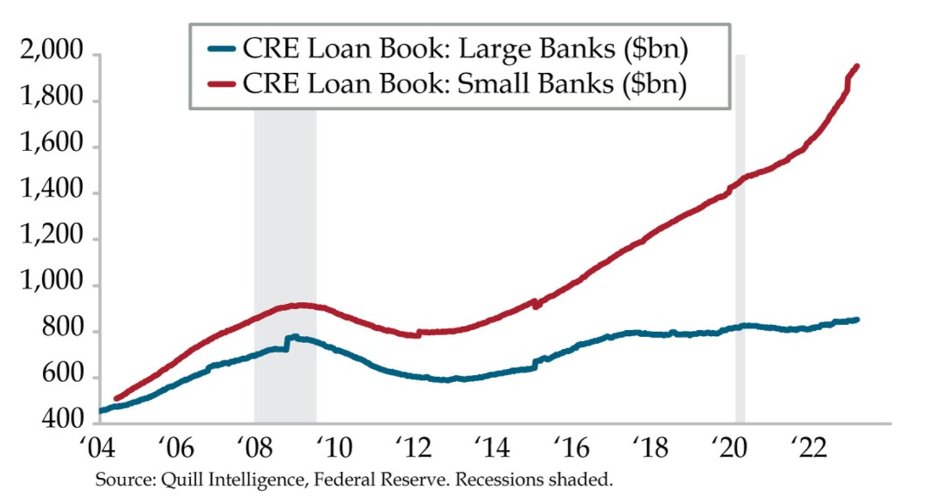

Commercial Real Estate debt investors today are HIGHLY CONCENTRATED.

Small banks hold *80%* of CRE loans worth $2.3T.

Once defaults start piling in, the US banking sector and all its stakeholders will be F*CKED…

How We Got Here

In 2022, US banks went on a frenzied buying spree for CRE. Loan exposure increased $4.8T to $5.3T, 4x the rate of years prior!

Why?

Back in ’21 rates were 0% & hikes imminent. Many CRE loans promise floating rate returns.

Result: banks unanimously said BUY!

This frenzied buying was much worse at SMALL banks than big.

Borrowing as a % of reserves shot from 25% to 95% YoY (Feb 2023)

…versus, this same metric only increased to 35% for big banks.

Key Operating Metrics — When & How to tell if Commercial Real Estate is in trouble

1. Discount/premium to NAV:

– for a $20T industry, if current asset values fall 10% across the board, that’s $2T in loss!

– who’s gonna pay? –> govt bailout

2. NOI:

– “net operating income”

– calculated by subtracting operating expenses from gross income

– deterioration here suggests problems with occupancy rates and/or rent collection and/or tenant quality

3. DSCR

– “debt service coverage ratio”

– a property’s ability to pay debts

– decline in DSCR means cash flow problems & is often the next symptom after decline in NOI

– problems here –> default

4. Occupancy rate

– duh, no tenants = no cash flow coming in

– in general a good occupancy ratio is ~90%

– in SF & NYC: current office space sector has 44% occupancy ????

5. Cap rate

– equal to NOI/ Property Value

– essentially: the rate of return for equity investors

Chart below contains a comprehensive list of all key operating metrics & who cares to measure each of them.

Current Market Forces Impacting CRE Market

a. Rate hikes:

– EFFR is now 4.8%. In mid-2021, this was 0%.

– Let me break down the effect of a rate hike explicitly: CRE loans come in 2 flavors only: either fixed rate or floating rate.

– Hike kills fixed rate NAV b/c bondholders still getting low coupons while the market is +480bps.

– Hike kills floating rate NAV b/c tenants can’t afford the new interest & default risk skyrockets.

b. WFH / COVID:

– this obviously destroyed occupancy rates across the country

– 2023 occupancy rates at a glance:

Austin: 66% of pre-pandemic levels

NYC: 47%

SF: 44%

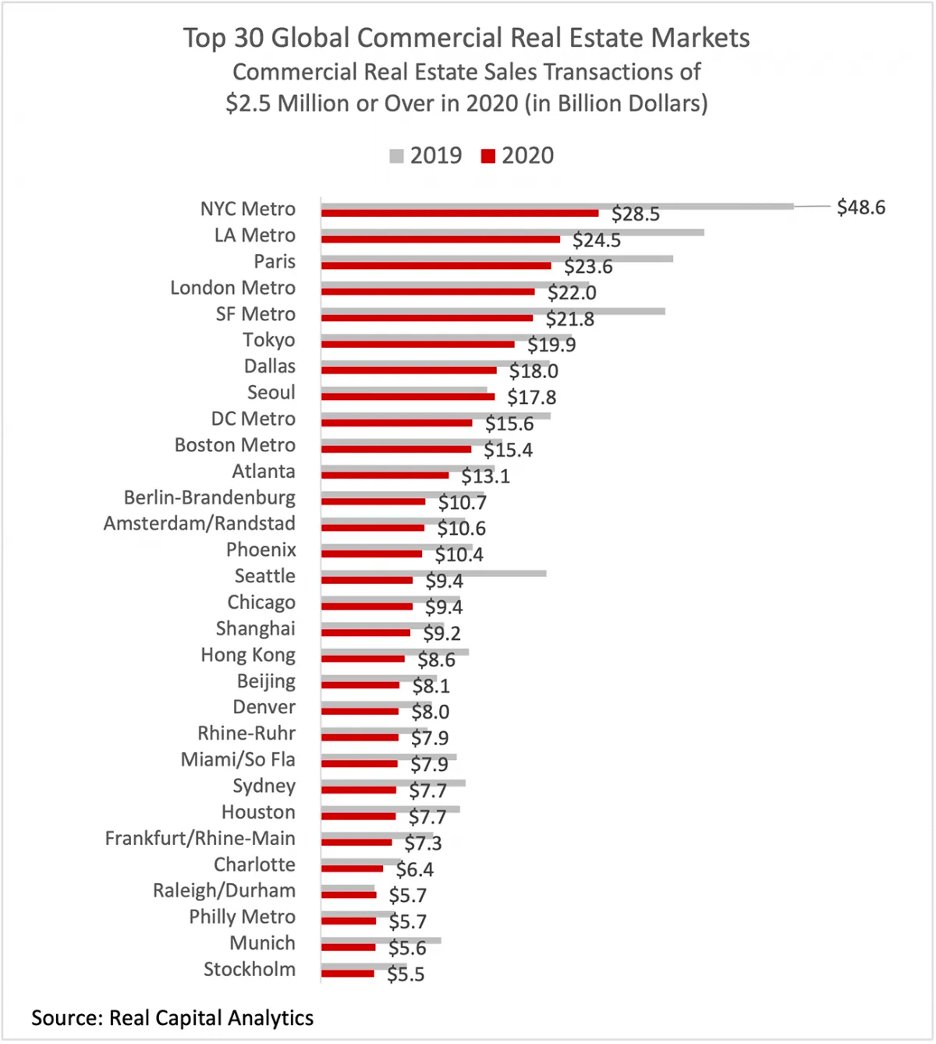

In major cities, CRE sales transactions plummeted almost 50% from 2019 to 2020 & they haven’t picked up since.

What’s Ahead: Defaults… Cascading Defaults

So far in 2023:

– Feb: Brookfield, #1 largest office owner in LA defaulted on $784M

– March: Pacific Investment Mgmt Co. defaulted on $1.7B of mortgage notes on 7 assets

– also March: Blackstone defaulted on $562M in Nordic CMBS

This is just the tip of the iceberg.

Breaking:

– Current value of loans & securities held by banks is $2.2T lower than the book value recorded on their balance sheets

– 10% of banks have larger unrecognized losses than those at SVB

– even if only half of uninsured depositors decide to withdraw, 190+ banks are at risk of $300B of insured deposits at risk.

Top CRE Lenders at Risk

Note: the watchlist below only ranks banks by absolute value exposure to the $2.2T of unrealized losses…

Small regional banks have less absolute exposure but may carry much higher exposure relative to their equity value.

Summary:

– While a single $1.7B commercial mortgage default in March 2023 may have spooked markets, this is a bellwether for many more to come.

– Investors & policymakers need to understand the contagion risk of the CRE loan crisis for & beyond US banks before its too late.