Michael Burry is one of the most popular value investors in the game. He’s a contrarian that buys odd-ball, roadkill stocks that others don’t. I dissected his seven write-ups from Value Investors Club to see how he analyzed stocks. A thread on the five lessons I learned…

Lesson 1: Burry Loves Small/Micro-Cap Stocks. The average market cap of the seven stocks Burry featured: $132M. There are a couple reasons Burry likes this space:

- Often highly illiquid

- Ignored by most investors

- Most think they’re frauds/sketchy biz Roadkill baby!

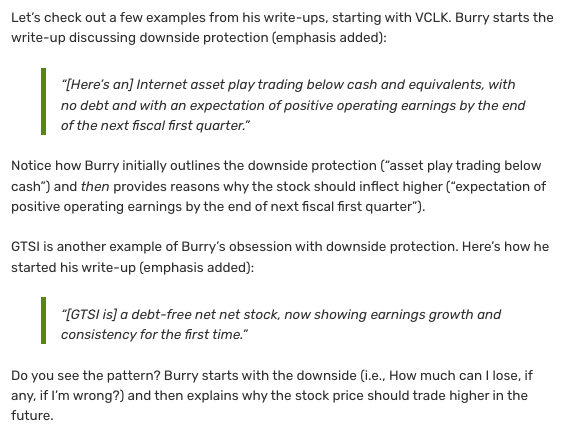

Lesson 2: Burry Emphasized Downside Protection. First most of the companies Burry highlighted had a few common characteristics:

- Trading at or below cash

- Little-to-no debt

- Massive discount to asset values

This protected him from losing 100% of his investment.

Lesson 3: Burry Likes Low Share Counts

Here are a few reasons why investors like Burry want low share counts:

- History of not diluting shareholders

- More illiquid

- Management doesn’t view its shares as cheap currency

- Lower prob. of future dilution

Lesson 4: Burry Cares About Absolute Value

Burry bought absolutely cheap stocks. He didn’t care about relative value. His wanted his stocks to be screaming cheap regardless of an industry comparison.

Cheap means:

- < 3x earnings

- < 5x FCF

- < 0.5x Book

- < 0.10x sales

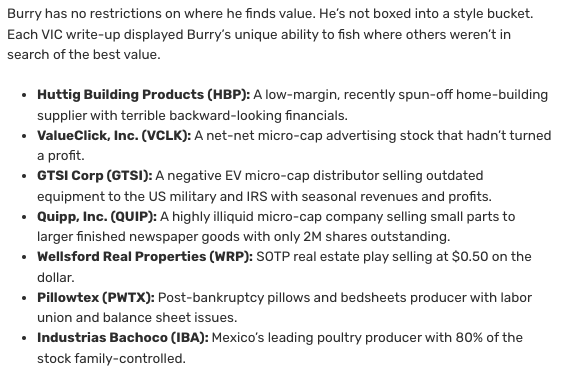

Lesson 5: Burry Was a Global Investor

It didn’t matter the industry or country. If it was cheap enough, Burry would write about it/invest. What I loved about Burry’s VIC write-ups was how diverse the ideas were: Distributors, poultry co’s, pillow makers, real estate. Unreal.

Recap: Lessons From Burry’s Investment Strategy Analysis

- Hunt in small/micro-cap space

- Focus first on downside protection

- Invest in businesses w/ low share counts

- Focus on ABSOLUTE vs. RELATIVE cheapness

- Kill all restrictions on finding cheap stocks